In today’s economy, processing transactions can not possibly be limited to face-to-face retail interactions, as customers use various devices to shop and pay for their purchases. As the demand for more convenient payment solutions rises, businesses introduce new ways to accept and process payments to stay competitive. As electronic devices become more and more ingrained with our day-to-day lives, companies look for technology solutions that can provide answers to their business needs.

Today, a good majority of businesses use a customer relationship management software or an accounting system to process payments when manual payment transaction via physical terminals is not an option. Aside from the convenience the integrated payment processing solution can provide, the enhancements in security of data being transferred is a huge plus for today's businesses.

Microsoft Dynamics CRM is becoming a popular business application for many businesses due to a variety of reasons.

The system is unique in the CRM marketplace and is leading the way in innovation and usability across the globe. The Dynamics CRM platform offers companies a unique set of productivity tools across sales, marketing, and customer service. Microsoft CRM is differentiated from competitors by its ability to extend and scale across multiple business units, giving companies the ability to leverage their Microsoft CRM investment without the need for additional software.

While there are a number of add-ons and plugins developed to enhance the CRM functionality or to add a new capability, there are not many payment applications designed to facilitate the processing of electronic payments inside Microsoft Dynamics CRM.

The main three contenders in this space are:

Century Business Solutions: eBizCharge

Powerobject: PowerCharge

Nodus Technology: CRMcharge

While all three provide payment processing capabilities within Microsoft Dynamics CRM, there're some minor differences among them that are worth looking at: both PowerCharge and CRMcharge allow you to accept payments inside your Dynamics CRM. However, both companies provide nothing beyond the processing capability. In other words, you will not have a merchant account and your transactions are processed through a third part, usually the company that provides the gateway to you. While this can be a good option for some businesses, many companies do not find it convenient to deal with two or three vendors when it comes to managing one task.

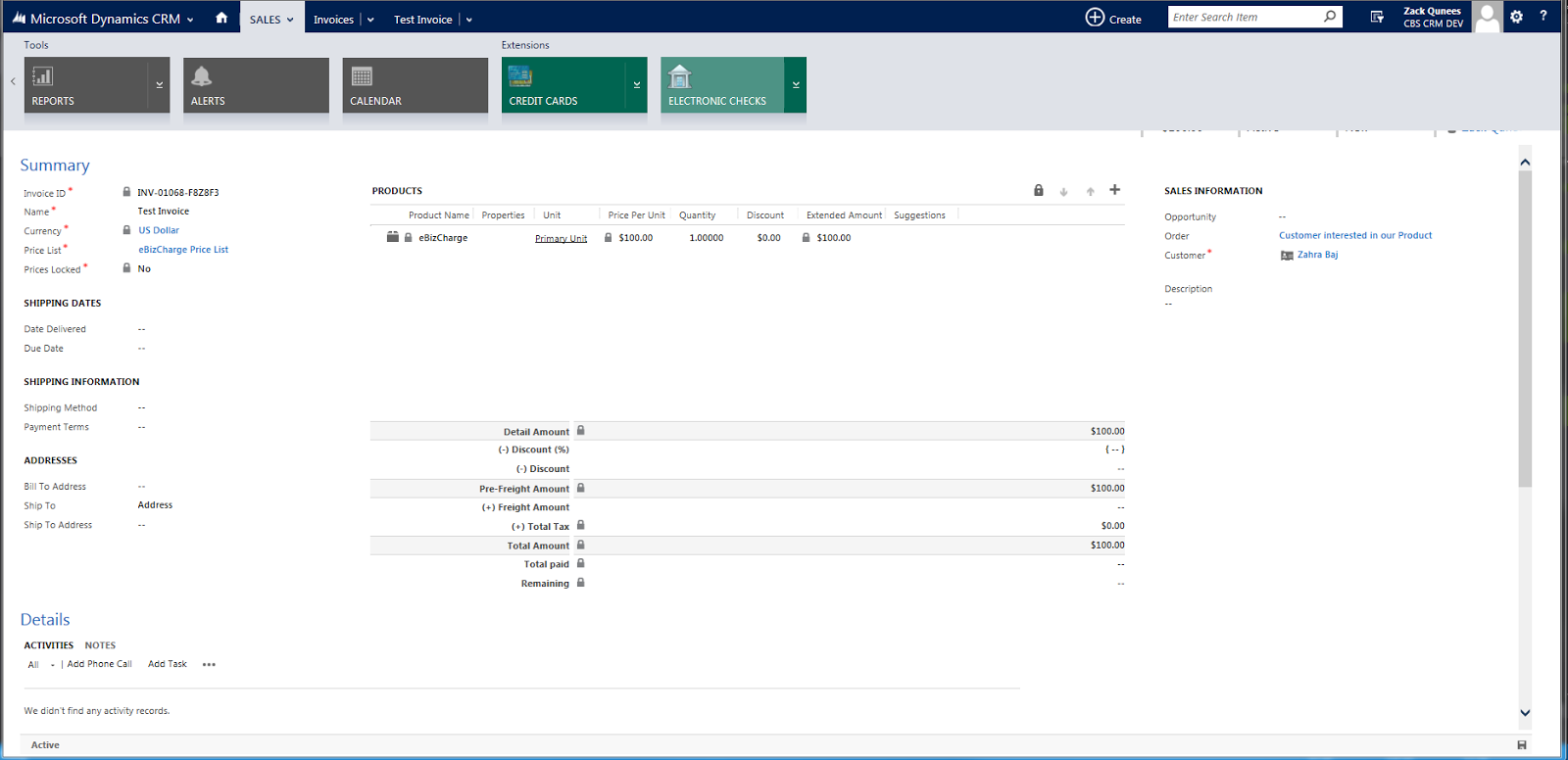

Century Business Solutions' eBizCharge, on the other hand, is the company's own gateway enhancement solution for Dynamics CRM. Century Business Solutions is a payment processor that handles the entire process for you from signing up for a merchant account to further customizing their integration to cater to your business's specific needs.

eBizCharge for Micosoft Dynamics CRM allows you to accept cards and use Century's processing services to take advantage of their cost-effective payment processing packages with dedicated account managers. The company provides in-house support and free charge-back management services to all their clients. Last but not the least, their solutions are FREE and they offer flat rate processing plans to make it easy and cost-effective to process payments within Dynamics CRM.

Introduced as a way for merchants to process their credit cards in an easy and simple way, Tier Pricing has been criticized by credit card experts, because it doesn’t provide any details or flexibility regarding credit card processing fees. Another common problem in Tier Pricing, is the mismatching of cards and rates. For example: A credit union debit card (usually a very low interchange rate type) can be billed to the merchant using a rewards card rate (one of the most expensive) transaction. This mismatching is legal and happens all the time. The reason has to do with the lack of variety (or categories) offered in Tier Pricing.

Introduced as a way for merchants to process their credit cards in an easy and simple way, Tier Pricing has been criticized by credit card experts, because it doesn’t provide any details or flexibility regarding credit card processing fees. Another common problem in Tier Pricing, is the mismatching of cards and rates. For example: A credit union debit card (usually a very low interchange rate type) can be billed to the merchant using a rewards card rate (one of the most expensive) transaction. This mismatching is legal and happens all the time. The reason has to do with the lack of variety (or categories) offered in Tier Pricing.