The best SAP Business one Finance Modules

SAP Business One is well respected as a flexible and powerful accounting solution in its own right. However, third-party plug-ins or add-ons, can often dramatically increase productivity within existing SAP Business One modules. The following finance plug-ins have been officially certified by SAP and are some of the best available for SAP Business One.

Accounts Receivable: Achieve AR Collections

A powerful application designed to facilitate credit and collections tasks, Achieve AR features a configurable order and credit approval system, is capable of monitoring payment trends, and can expose potential credit risks. The application can automatically “hold” placed orders that do not pass customizable credit checks, reducing financial losses within an organization. The add-on also allows collection notices to generate and dispatch automatically once an invoice has gone unpaid after a user selected timeframe.

Credit Card Processing: eBizCharge

A versatile payment add-on, eBizCharge for SAP B1 is a SAP certified payment application capable of processing a wide array of credit, debit, and ACH payments inside SAP B1. eBizCharge is PCI-compliant and utilizes the latest data encryption and tokenization technology for maximum security. Century Business Solutions offers the payment processing solution as well as processing services, resulting in an overall lower processing costs and better support experience for SAP B1 users.

Asset Management: FAMe

A robust asset management enhancement, FAMe brings flexible management options to equipment financing, asset maintenance, and lease & rental accounts. Various application components can be easily disabled at the initial set-up, allowing an organization to grow into the expansive features as needed, providing a highly customizable user experience. An asset tracking feature keeps users informed at all times and an asset financing option provides detailed reporting on loans, leases and rentals. FAMe also synchronizes contracts and work orders automatically within the SAP Business One financials module, making asset related expenses easily predictable and manageable.

Project Management: MARIProject

A real-time project management tool, MARIProject (formerly known as ProjectManagement based on SAP Business One) provides easily accessible project data and allows detailed reporting on purchasing, partner information and other crucial project related details. The resource planning feature allows a user to drag-and-drop employees or contractors into specific projects, allowing accurate project budgeting and organization based on an individual’s capacity and cost. As an added convenience, all of the MARIProject features and benefits are fully accessible from mobile devices.

Documents: EDI DOCMAN

By proving reliable and secure access to EDI/EC documents, both in and out of SAP Business One, EDI DOCMAN brings reliability and user friendliness to EDI related tasks. Application benefits include EDI document tracking and the ability to import and export documents individually or grouped together. EDI DOCMAN also features document correction and rejection functionality, and provides a comprehensive EDI checklist- ensuring all docs are fully EDI complaint before being sent.

Wednesday, January 6, 2016

Wednesday, December 30, 2015

How to process payment transactions inside Microsoft Dynamics CRM

Accepting electronic transactions with Microsoft Dynamics CRM

In today’s economy, processing transactions can not possibly be limited to face-to-face retail interactions, as customers use various devices to shop and pay for their purchases. As the demand for more convenient payment solutions rises, businesses introduce new ways to accept and process payments to stay competitive. As electronic devices become more and more ingrained with our day-to-day lives, companies look for technology solutions that can provide answers to their business needs.

Today, a good majority of businesses use a customer relationship management software or an accounting system to process payments when manual payment transaction via physical terminals is not an option. Aside from the convenience the integrated payment processing solution can provide, the enhancements in security of data being transferred is a huge plus for today's businesses.

Microsoft Dynamics CRM is becoming a popular business application for many businesses due to a variety of reasons.

The system is unique in the CRM marketplace and is leading the way in innovation and usability across the globe. The Dynamics CRM platform offers companies a unique set of productivity tools across sales, marketing, and customer service. Microsoft CRM is differentiated from competitors by its ability to extend and scale across multiple business units, giving companies the ability to leverage their Microsoft CRM investment without the need for additional software.

While there are a number of add-ons and plugins developed to enhance the CRM functionality or to add a new capability, there are not many payment applications designed to facilitate the processing of electronic payments inside Microsoft Dynamics CRM.

The main three contenders in this space are:

Century Business Solutions: eBizCharge

Powerobject: PowerCharge

Nodus Technology: CRMcharge

While all three provide payment processing capabilities within Microsoft Dynamics CRM, there're some minor differences among them that are worth looking at: both PowerCharge and CRMcharge allow you to accept payments inside your Dynamics CRM. However, both companies provide nothing beyond the processing capability. In other words, you will not have a merchant account and your transactions are processed through a third part, usually the company that provides the gateway to you. While this can be a good option for some businesses, many companies do not find it convenient to deal with two or three vendors when it comes to managing one task.

Century Business Solutions' eBizCharge, on the other hand, is the company's own gateway enhancement solution for Dynamics CRM. Century Business Solutions is a payment processor that handles the entire process for you from signing up for a merchant account to further customizing their integration to cater to your business's specific needs.

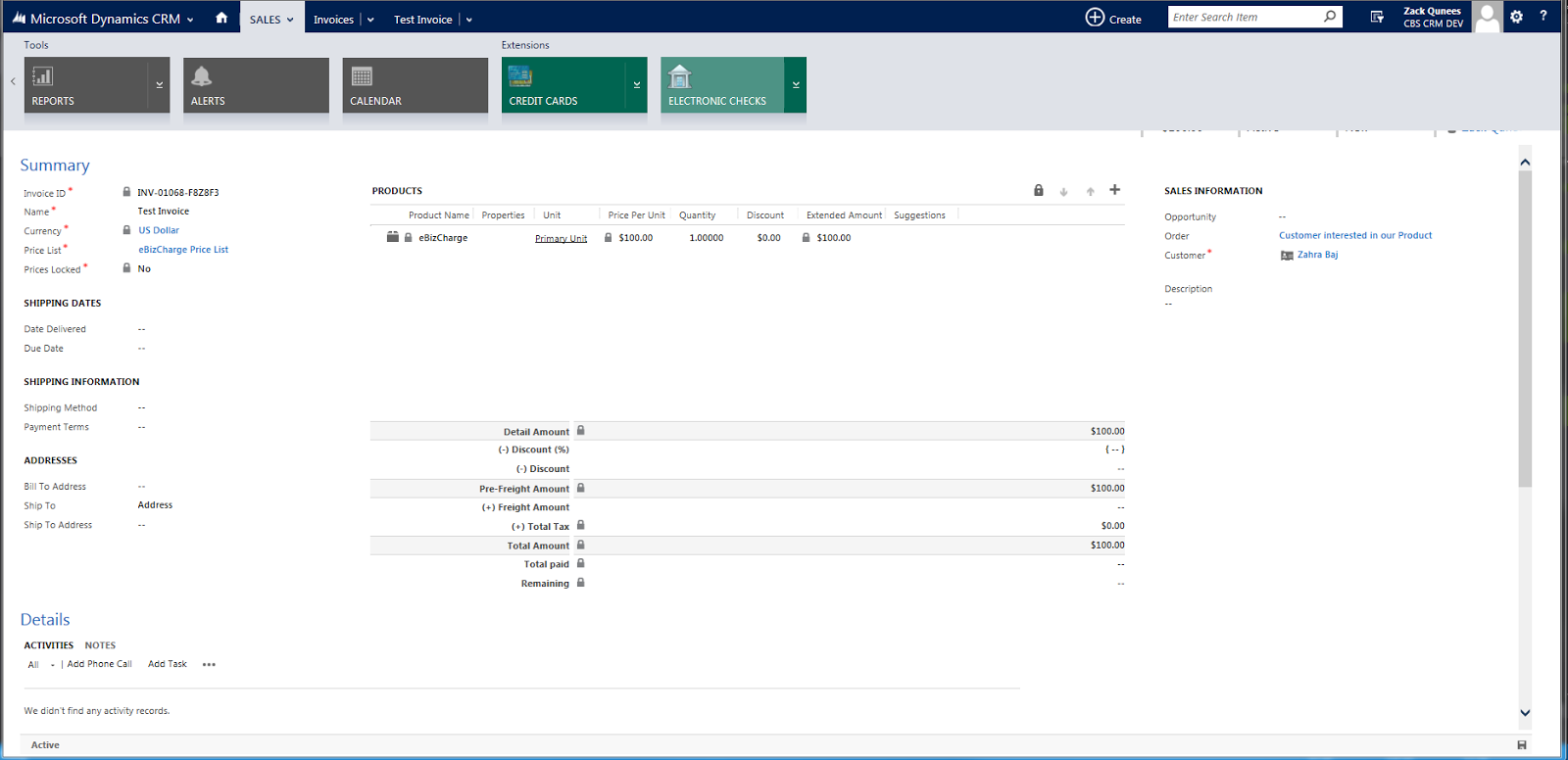

eBizCharge for Micosoft Dynamics CRM allows you to accept cards and use Century's processing services to take advantage of their cost-effective payment processing packages with dedicated account managers. The company provides in-house support and free charge-back management services to all their clients. Last but not the least, their solutions are FREE and they offer flat rate processing plans to make it easy and cost-effective to process payments within Dynamics CRM.

In today’s economy, processing transactions can not possibly be limited to face-to-face retail interactions, as customers use various devices to shop and pay for their purchases. As the demand for more convenient payment solutions rises, businesses introduce new ways to accept and process payments to stay competitive. As electronic devices become more and more ingrained with our day-to-day lives, companies look for technology solutions that can provide answers to their business needs.

Today, a good majority of businesses use a customer relationship management software or an accounting system to process payments when manual payment transaction via physical terminals is not an option. Aside from the convenience the integrated payment processing solution can provide, the enhancements in security of data being transferred is a huge plus for today's businesses.

Microsoft Dynamics CRM is becoming a popular business application for many businesses due to a variety of reasons.

The system is unique in the CRM marketplace and is leading the way in innovation and usability across the globe. The Dynamics CRM platform offers companies a unique set of productivity tools across sales, marketing, and customer service. Microsoft CRM is differentiated from competitors by its ability to extend and scale across multiple business units, giving companies the ability to leverage their Microsoft CRM investment without the need for additional software.

While there are a number of add-ons and plugins developed to enhance the CRM functionality or to add a new capability, there are not many payment applications designed to facilitate the processing of electronic payments inside Microsoft Dynamics CRM.

The main three contenders in this space are:

Century Business Solutions: eBizCharge

Powerobject: PowerCharge

Nodus Technology: CRMcharge

While all three provide payment processing capabilities within Microsoft Dynamics CRM, there're some minor differences among them that are worth looking at: both PowerCharge and CRMcharge allow you to accept payments inside your Dynamics CRM. However, both companies provide nothing beyond the processing capability. In other words, you will not have a merchant account and your transactions are processed through a third part, usually the company that provides the gateway to you. While this can be a good option for some businesses, many companies do not find it convenient to deal with two or three vendors when it comes to managing one task.

Century Business Solutions' eBizCharge, on the other hand, is the company's own gateway enhancement solution for Dynamics CRM. Century Business Solutions is a payment processor that handles the entire process for you from signing up for a merchant account to further customizing their integration to cater to your business's specific needs.

eBizCharge for Micosoft Dynamics CRM allows you to accept cards and use Century's processing services to take advantage of their cost-effective payment processing packages with dedicated account managers. The company provides in-house support and free charge-back management services to all their clients. Last but not the least, their solutions are FREE and they offer flat rate processing plans to make it easy and cost-effective to process payments within Dynamics CRM.

Thursday, December 3, 2015

Interchange Plus Pricing vs Tier Pricing

Interchange Plus Pricing vs Tier Pricing

Interchange Plus Pricing

Pros:

-The cheapest processing option overall.

-100 % clarity on all processing costs.

-More understanding of different card rates.

-Flat fees mean no surprises.

Cons:

-Takes some time to learn the different processing rates for each type of credit cards.

-Requires you to be more involved in your day-to-day card processing.

Tier Pricing

Introduced as a way for merchants to process their credit cards in an easy and simple way, Tier Pricing has been criticized by credit card experts, because it doesn’t provide any details or flexibility regarding credit card processing fees. Another common problem in Tier Pricing, is the mismatching of cards and rates. For example: A credit union debit card (usually a very low interchange rate type) can be billed to the merchant using a rewards card rate (one of the most expensive) transaction. This mismatching is legal and happens all the time. The reason has to do with the lack of variety (or categories) offered in Tier Pricing.

Introduced as a way for merchants to process their credit cards in an easy and simple way, Tier Pricing has been criticized by credit card experts, because it doesn’t provide any details or flexibility regarding credit card processing fees. Another common problem in Tier Pricing, is the mismatching of cards and rates. For example: A credit union debit card (usually a very low interchange rate type) can be billed to the merchant using a rewards card rate (one of the most expensive) transaction. This mismatching is legal and happens all the time. The reason has to do with the lack of variety (or categories) offered in Tier Pricing.

In Tier Pricing, all transactions are billed under just a handful of general categories, usually four:

-Debit aka. Check Cards

-Qualified (standard credit cards)

-Mid-Qualified (hand typed cards such as phone orders/mail orders)

-None Qualified (rewards cards, international cards, etc.)

Since there are no set rules or guidelines determining what cards will go under each category. Mismatching often occurs, and leads to millions of dollars being over charged to merchants per year.

Pros:

-A simple introduction to payment processing for the novice merchant.

-Minimal time commitment from the merchant.

– Zero learning curve.

Cons:

-Results in much higher processing costs overall.

-No details on what exactly the merchant is paying for.

-Zero understanding of industry card pricing.

Interchange plus vs. tiered pricing model. Which is better?

I strongly recommends Interchange Plus pricing, even to novice merchants. The enormous benefits over Tier Pricing, make switching to Interchange Plus pricing a smart business decision. As discussed, Interchange Plus provides merchants complete transparency, as well as the ability to easily analyze and understand their exact processing costs. This detailed information also allows the merchant to compare pricing programs among different merchant service providers. Of course, the biggest benefit of Interchange Plus pricing is it provides merchants a lot of flexibility, beyond the limitations of Tier Pricing. How? By not narrowing down so many different card types into just a handful of generic categories, transactions get processed more accurately- which leads to much lower processing rates on corporate, commercial, business, government, and purchasing cards. This benefit alone, leads to thousands of dollars in savings per year.

Monday, October 19, 2015

Wednesday, April 22, 2015

Why Data Security Concerns Small Businesses

Why Data Security Should Concern Small Businesses (and All Businesses, Really)

Given the culture of mainstream data security breaches we’ve

been unwittingly thrust into beginning in about 2013, I think it goes without

saying that PCI compliance is vitally important, not just in the world of

payment processing, but in the world of business in general.

Oh, PCI compliance… I’m talking about that item that never

fails to pop up on your credit card processing statement. It’s that one thing you’re always billed for,

no matter whether it’s in the positive (PCI

compliance fee) or the negative (PCI

noncompliance fee). Funny little

line item it is.

For some business owners, that’s all it will ever be –

another annoying, unexplained little line item in an entire world of more

pressing business issues. Maybe something a bit

like car insurance – an expense whose worthiness won’t be proven until the day

of a catastrophic, metal-twisting wreck.

As a business owner, does a data security breach as you grow your business really concern someone

like you? Or, is this just a game the

giants play while anyone smaller than Goliath watches from the bleachers?

Lately, all signs seem to say that yes, business owners – even small business owners – ought to be quite

concerned with data security breaches.

Breaches are actually down

worldwide from two years ago, but, as our buying culture moves slowly but

surely to credit from cash (and our general habits from physical to online),

fraudsters and hackers see the channel as a very viable road to profit. Although PCI noncompliance is just one cause

of data security breaches, taking a look at compliance and general payment security pointers can benefit all business

owners, as security flaws are usually extremely correctable.

This piece isn’t meant to alarm you; instead, it’s more of a

wake-up call for businesses who’ve relegated PCI compliance to the back burner –

or, didn’t put it on the stove at all.

Better at least cover that pot if you’re keeping it out overnight.

So, what is PCI compliance, then?

Basically, it’s the security of credit card information –

that is, how safe you’re keeping it when and if you’re storing it.

Some aspects of PCI compliance are thoroughly under your

control. For example, when faced with

the decision of whether or not to copy down a customer’s credit card number to

enter into your accounting system or credit card terminal later, you can choose

not to, knowing well that paper trails, even destroyed ones, can increase your

fraud liability.

And, other aspects are thoroughly out of your control. For example, you may be using a payment

processing program that keeps unprotected credit card information stored on

your business’ server (and, though it sounds crazy, there are programs that do

just that).

Do you have a Target (or a Home Depot) on your back?

It’s an unfortunate circumstance of today’s media coverage

that the big guys get most (if not all) of the attention, while the little guys

get next-to-nothing. Contrary to what

you may have heard, small businesses are a favorite target for hackers. This white

paper shows that 70% of all reported data security breaches happen in small

businesses – a truly incredible, harrowing statistic, telling a much different

story than the one you’d understand by only reading headlines.

The headline stories make sense; compared to the enormity of

the Target and Home Depot data breaches, the small business ones are…well, quite

small. Though they may be small enough

to dip underneath the radar completely, they’re certainly a big story to the

business owners they affect.

Data breaches can be murder

I don’t mean for you as a person, obviously. But, to your business? That’s a yes.

The National

Cyber Security Alliance stated in a report that when a small business is

hacked and has its customers’ information compromised, it has a 60% chance of

closing its doors within six months of the attack.

When you look at that statistic in tandem with the

aforementioned one about how 70% of all reported data breaches occur in small

businesses, it’s not quite a death sentence for small businesses – but, it’s

close.

Especially in our age, hackers and fraudsters are more

skilled than ever before, and, they’re very aware of the fact that small business

owners think they’re too small to be viable targets for information

breaches. Incidentally, they’re also too

small to be seen by most anyone when they’re broken into, so nobody ever thinks

to change their own security tactics until ex post facto.

Don’t be the next unseen statistic

You don’t have to be another story nobody hears about. Now that you know about all this negativity,

you’ll be quite pleased to know it’s not difficult at all to protect yourself

from invisible hackers and others who don’t have your best interests in mind.

Regardless of security breaches caused by hackers, it’s

pretty easy for anyone to straighten out a rumpled piece of paper you used to

copy down someone’s credit card number.

Indeed, this isn’t what most people think of when they hear that term data breach, but if anyone recovers that

trashed piece of paper you used, you’ll be liable for any consequences that may

arise just the same. Just resist the

urge to engage in that practice, and, if you’ve absolutely needed to do so in

the past (for business procedures, direct orders, or any other reason), it may

be time to revise standard procedure.

Additionally, if you use a computer-based credit card

processing system that stores full, unprotected credit card numbers on your own

server (read: is not PCI compliant), it’s time to look into an updated

solution, something that fits today’s security standards. Solutions that employ tokenization technology, for example, break sensitive data into strings of random numbers when in storage, so anyone who successfully breaks into a server storing the information doesn't get anything worthwhile - only garbled strings of characters.

If you used a cloud-based processing system, for example,

you wouldn’t be liable for a data compromise the same way you would if you used

something that stored information on your own servers. If you aren’t sure about the status of your

own processing system (for example, where it stores information, whether or not

it’s even cloud-based), it never hurts to ask your credit card processor or

search for reviews of the product you use that relate to PCI compliance and

data security in general.

So, what is the

value of PCI compliance to small businesses?

It’s much more than a little line item on your statement; the very survival

of many businesses depends on it. Be

absolutely sure your own business maintains PCI compliance to avoid any

potential pitfalls, and rest easy knowing that your customers’ payment records

are safe because of something you did

for your business. Because, as a small

business owner, you’ve got a lot more to pore over than fretting about losing

your business because of an entirely avoidable data security lapse.

Thursday, April 16, 2015

There’s a New Payments Advocate in Town – and it’s the Government!

They've formed something called the CPTC - and, the PIC.

But... What do they do?

If you follow this blog, you know I’m all about electronic payments. But, I’ll bet you didn’t know that as of a month ago, the government is all about electronic payments, too!

It’s true. On March

19th, Washington issued a press

release announcing the formation of a new discussion group, the bipartisan Congressional

Payments Technology Caucus (CPTC). The bipartisan

caucus, headed by four US Representatives, will discuss how innovations in

payment technology affect all consumers, especially the segment of consumers

who aren’t tied to any physical bank, as well as data

security.

As well, on April 9th, four US Senators formed

the bipartisan Payments Innovation Caucus (PIC). Like the CPTC, the PIC will explore data

security trends, general payment

innovations, and how those innovations protect consumers.

Both the CPTC and the PIC exist not only to foster discussion

among congressmen, but to spread awareness of payments technology issues and,

in doing so, move contents of the discussions onto the appropriate law-making

forums.

What does this mean?

I say it’s about time Congress got on board with electronic

payments. I guess after years of

silently developing a hold on our collective hearts, first with simple credit cards, then with mobile payments and digital wallets - and then breaking many of them with those nasty data breaches - someone had to take notice.

It’s a very good thing, because according to

an article

from Senator Gary Peters (D-MI), a staggering 70% of consumer spending

happens electronically (although the difference between card payments and ACH

transactions isn’t specified). He says

that by 2017, consumers will be spending $7.3 trillion per year electronically. (For more stats on current usage as well as the advancement of payment security in general, you can check out this white paper, Payment Security and Beyond in 2015.)

So, does this mean law-makers will take action that involves

credit card payments and data security?

Will the government’s involvement in payments mean more support for

small businesses? A global shift in credit

card processing costs? All things

remain to be seen, and, since we’re talking about a government operation, we

can expect a snail’s pace. But, it’s

something.

Tuesday, April 14, 2015

Which is Worse: A Damaged Reputation or the Loss of a Key Employee?

Which is Worse: A Damaged Reputation or the Loss of a Key Employee?

|

| This man isn't sure yet...but he'll know soon enough. |

It’s an interesting juxtaposition.

Would your company suffer more from the loss of a key

employee, someone who hit his numbers every month, has an exemplary track

record with his clients, or whose visionary ideas helped shape the company – or

a tarnished reputation brought on by an unforgivable social gaffe or, worse, a data breach revealing the personal information of countless customers?

In order to examine this fully, we’ll need to break it down

into smaller pieces: The benefits of having a top-of-class employee working for

you, and the negative effects of losing such a person in your workforce. And, we’ll need to look at the payoff of

having a great reputation versus the deleterious effects of having a bad one.

Benefits Brought by a Key Employee

Having a good employee at your disposal obviously carries a

string of benefits.

The work he’s assigned gets done, and, not just that – it’s

meaningful to the company, so it ends up bringing in appreciable revenue,

revenue which certainly would not have arrived if that employee hadn’t

contributed his work.

Having such an employee can also mean entirely new ideas for

your company, from website tweaks that positively affect traffic and search

engine ranking to an entirely new, successful product line.

The possibilities are great.

Bad Effects of Losing that Key Employee

Conversely, what happens when that same employee that

created all the extra revenue and had ideas no one else could muster ends up

leaving your company?

Certainly you can ride on his ghostly laurels for a

time. But, after that time, you’ll start

to see a decrease in revenue because the production that key employee brought

to the table simply isn’t there.

In time, after the key employee leaves, you might have some vestigial

remains of his handiwork (such as that tweaked website you’ve told his

successor not to touch) or the new product line that someone else oversees, but

you won’t get the innovation back.

In short, you’ll return close to the productivity and

revenue levels you were at before. Your

current clients might not notice much – maybe a different voice on the phone –

but, you will.

Benefits Earned by a Great Reputation

Good reputation, on the other hand, can be thought of as

something that happens when you have a good employee working for you.

You garner a good reputation when someone visits the website

that your star employee helped revamp and has a much easier time checking out

and paying for his order. He might tell

his friends how easy it was, and he might even mention how you seem to have

diversified your product lines, too. He

might write a review on Yelp, for that matter.

But, the principle is the same. Good

reputation comes from people saying good things about you.

The good thing about good reputation is it outlasts your

star employees. Whereas your influx of

keen ideas might slow to a halt if your star producer leaves, people will

remember how they felt when they read his work, when they surfed on his

website, or when they bought the products he conceived of. And, they’ll come back for more.

Negative Effects of a Bad Reputation

And, conversely, as good as the effects of a sparkling

reputation can be, the effects of a lousy one can be exactly as bad. And, usually worse.

You might inadvertently plant a seed of bad reputation by

making a faux pas at a large social gathering for your business. By comparison, you might plant a sequoia grove

by inadvertently compromising your customers’ data in a data breach.

Now, we’ve all read negative reviews on Yelp. Those reviews are the ones that seem to stick

the most, and the ones that seem to arouse the most passion. Without going into the psychology behind it,

let it suffice to say bad reputation is a much bigger worry than good

reputation is a boon. Whereas people

interpret your good reputation to mean you’ve done mostly good things, people

usually interpret a bad reputation to mean anyone’s given experience with you

will be unequivocally bad. No bones about it.

And, what’s more is the fact that a good reputation can

easily shift to bad, but a bad

reputation has a much harder time turning over to good once more. A bad reputation outlasts your star employees and your bad apples, too.

So, Which is Worse? Losing a Key Employee or a Damaged Reputation?

After reading this article, hopefully the answer is clear as

day.

Losing an essential employee might look bad on paper, but

you’ll not only retain a good deal of his innovations (in some cases), but you

won’t be thought of negatively just

because of his loss. You might be

thought of…not quite as well. But, not

badly.

If your reputation’s tarnished, though, forget about it.

Negative reviews on Yelp live on forever, and people glom

onto those juicy, bad stories much more than they do positive ones. I mean, what captivates us when we read

books? See movies?

It’s the conflict. It

excites us. We can use it to our

advantage, of course (for example, avoiding a place that has horrid reviews on

Yelp), but that doesn’t change the fact that we’re drawn to it.

That’s just how it is.

How Can You Protect Yourself?

Believe it or not, this article shouldn’t read like a death

sentence. It’s very possible to garner a

good reputation and keep it that way.

You just have to be smart.

If that means calculating more heavily what you say in

social situations, so be it. If it means

turning the other cheek when someone calls you a name instead of flying off the

handle, you can handle it. If it means

investing time into looking into a tokenized security solution - or any number of other data security measures - for your

customers’ secure information, it’s worth looking into.

Subscribe to:

Comments (Atom)